(Seoul=Yonhap Infomax) Eun Byul Yun – South Korea Gas Corporation (KOGAS) is facing mounting concerns as a significant portion of its short-term debt matures at the end of the year.

The situation is exacerbated by a sharp rise in short-term interest rates and the typical year-end liquidity squeeze in local markets, raising the risk of challenging refinancing conditions.

According to Yonhap Infomax’s integrated statistics on commercial paper (CP) and electronic short-term bonds (screen no. 4717) as of the 25th, KOGAS’s outstanding short-term debt—including CP and electronic short-term bonds—stood at 5.14 trillion won ($3.9 billion).

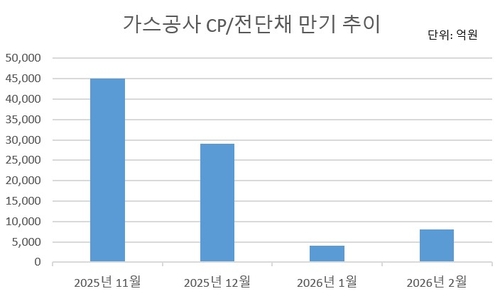

Notably, more than 3 trillion won ($2.3 billion) of this debt is set to mature by year-end. Yonhap Infomax’s issuer-specific bond maturity statistics (screen no. 4290) show that KOGAS faces 3.18 trillion won ($2.4 billion) in short-term debt maturities before the end of the year.

KOGAS typically increases short-term borrowing during the winter, when gas demand rises and working capital needs grow due to delayed accounts receivable collection. However, the company has been reducing its year-end short-term borrowings compared to previous years. In the same period last year, maturing short-term debt reached approximately 6.7 trillion won ($5.1 billion).

Amid shifting monetary policy expectations, bond yields have surged and credit market sentiment has cooled. The yield on 91-day CP jumped from around 2.7% at the end of last month to 2.96% as of yesterday. If KOGAS rolls over all maturing debt at these higher rates, its additional interest burden could amount to several billion won.

Concerns are heightened by the seasonal year-end liquidity contraction. Over the past five years, short-term rates—including CP—have consistently risen from October to December.

Recent KOGAS issuances also reflect this trend, with coupon rates rising sharply compared to two or three months ago. For example, CP maturing in March 2025 issued on the 19th carried a coupon rate in the 3% range, up from 2.6–2.7% for three-month notes issued in September and October.

However, there are signs of stabilization in both the bond and short-term funding markets. One bond market participant noted, “The short-term market had been under significant pressure, but we’re seeing some recovery. Still, CP rates backed by time deposits remain elevated, so we need to monitor the situation further.”

KOGAS is also gradually reducing its debt burden to improve its financial structure, raising the possibility of cash repayment or alternative funding methods.

As of Q3 this year, KOGAS’s other borrowings—including CP, electronic short-term bonds, and bank loans—fell by about 37% quarter-on-quarter to 8.2041 trillion won ($6.2 billion). In contrast, outstanding corporate bonds, including foreign currency bonds, rose about 3% to 27 trillion won ($20.4 billion) during the same period.

A KOGAS official said regarding year-end CP and electronic short-term bond refinancing, “We will make decisions based on market conditions and are reviewing various funding options.”

ebyun@yna.co.kr

(End)

Copyright © Yonhap Infomax Unauthorized reproduction and redistribution prohibited.